Conventional business models and traditional ways of doing business are under constant threat in the current age of technological disruption. Few insurers will remain unaffected by determined new firms that are harnessing the power of innovative technologies to uproot longstanding market leaders.

“Modern insurers are increasingly leveraging data from internet of things sensors and applying powerful artificial intelligence (AI) algorithms to deliver just-in-time risk warnings through true omnichannel interactions on an unprecedented scale,” says Tony Tarquini, European insurance director at software company Pegasystems.

“The quality of protection delivered through risk-warning services and suggested solutions to the risk will be the most important differentiating factor for any insurer and therefore be the key to business success.”

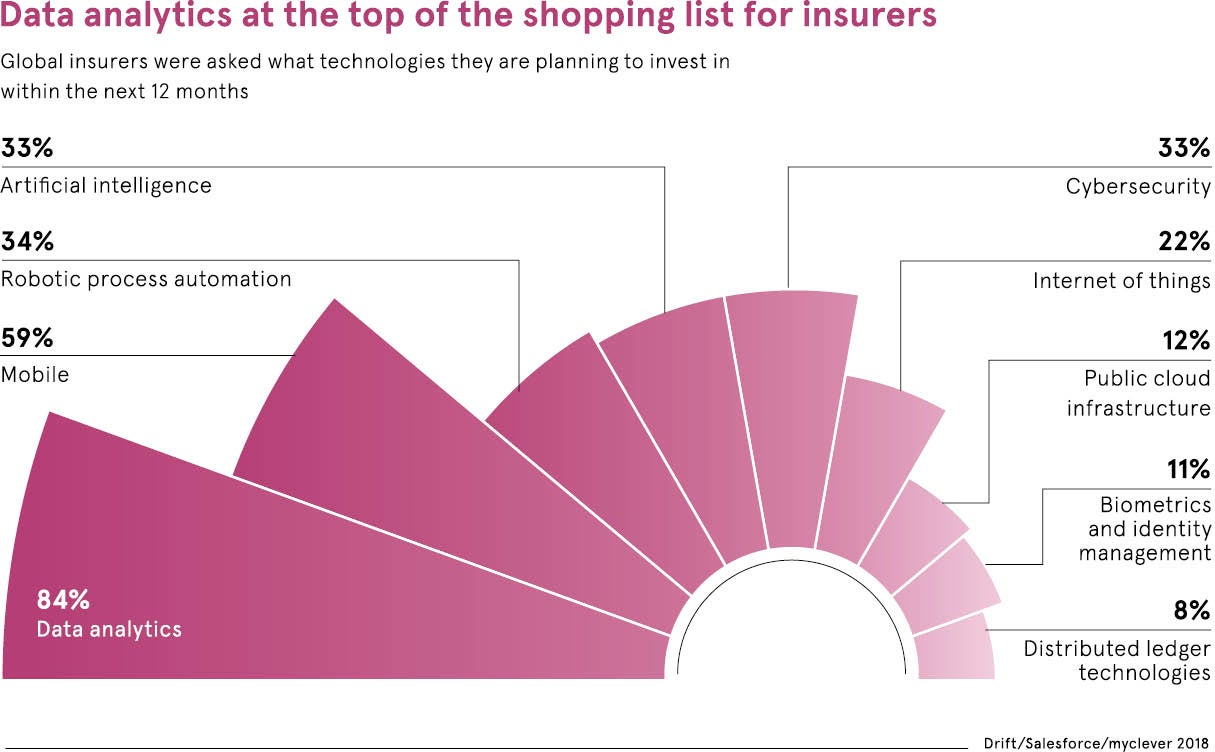

Advanced AI, machine-learning tools and big data analytics are giving insurers the power to move into the predictive cover. As the amount of customer data available to insurers increases, they will be able to exploit this high-quality information to forecast consumer behaviour accurately and provide personalised feedback to reduce claims.

Multinational insurance firm Aviva is using predictive analytics to help policyholders minimise their risk of getting into road accidents through unsafe driving. Through the Aviva Drive app and advanced vehicle telematics technology, drivers will have their driving style assessed with safer drivers saving an average of £170 on their car insurance premiums. Providing a financial incentive for consumers to focus on better driving practices will alter their behaviour and, in turn, become lower risk for insurers.

“By utilising these techniques, insurers will be able to better understand customers and the risks and uncertainties they face. And with this enhanced understanding, insurers will have the opportunity to provide more tailored products and services, and help customers to understand, manage and reduce their own risk,” says Owen Morris, managing director of Aviva Quantum, Aviva’s data science practice.

The full potential of predictive analytics in insurance extends far beyond just any single industry or customer segment with the relationship between insurer and customer set to shift fundamentally. Not only will leading insurers interact more often with policyholders, to share ways to reduce risk, but they will also become adept at deploying innovative monitoring technologies to consumers, leading to lower costs for both parties.

Those who are fastest and best in leveraging predictive analytics can realise superior returns

“Better risk prevention through predictive analytics has a direct impact on claims expenses – those who are fastest and best in leveraging predictive analytics can realise superior returns, as in the long run better risk prevention also means the prices will come down. This is a very important capability for insurers to develop and those that don’t figure out how to leverage predictive analytics risk falling behind,” says Henrik Naujoks, partner and financial services practice leader for Europe, the Middle East and Africa at consultancy Bain & Company.

American insurance company Esurance is already using predictive analytics to speed up the processing of urgent claims after natural disasters. After Hurricane Harvey caused massive flooding damage in Texas, Esurance used predictive analytics to study aerial images of impacted areas captured from planes, so adjusters didn’t have to inspect vehicles physically.

American insurance company Esurance is already using predictive analytics to speed up the processing of urgent claims after natural disasters. After Hurricane Harvey caused massive flooding damage in Texas, Esurance used predictive analytics to study aerial images of impacted areas captured from planes, so adjusters didn’t have to inspect vehicles physically.

Insurers may be well aware of the benefits afforded by new technologies, but effectively implementing these tools can be a complex process. According to KPMG, 91 per cent of insurance company chief executives say they are worried about how to introduce automation, AI and cognitive robotics to their business models, with Mr Naujoks believing the challenges facing executives looking to embrace predictive analytics to be varied.

“Perhaps they have a sense of urgency but no strategic direction, or in some cases many potential applications but no systematic approach, and in other cases an ambitious agenda but little real progress,” he says.

“We have identified three critical components: insurers need to define a clear analytics strategy, make sure to set up an operating model to deliver business value with AI, and really make a commitment to invest in the build-up of data and analytics capabilities.”

Real-time data collection from the billions upon billions of sensors and connected devices gives insurers huge amounts of data that can be used to make strong forecasts and predictions of future consumer behaviour. From wearable sensors, supplying insight into health for life insurers, to smart sensors in the home, predicting when devices need repairing, the opportunities for insures that make the most of the next generation of technological innovation are immense.

The established business model that the vast majority of insurers still use today, which bases insurance premiums on simplistic questions around age, profession and gender, is unlikely to survive the widespread adoption of predictive analytics solutions.

“Tomorrow the model will be active, real-time risk management with 24/7 service interaction. If insurers don’t provide these services, they will be relegated to back-end claims payers, with tech companies stepping in to own the customer relationship and forever steal their distribution channels. This applies to virtually every line of business,” Pegasystems’ Mr Tarquini concludes.