A lot has changed since the coalition government came to power back in 2010, but there is one issue that is still a concern for many firms across the country.

It is that some British businesses, especially small and medium-sized enterprises (SMEs), are still struggling to access the funds they so desperately need in order to grow from the traditional lending routes since the financial crisis struck in 2008.

While there had been some promising signs last year that the traditional frozen lending routes had started to thaw, the latest available figures show 2015 ended on a negative note.

Lending slump

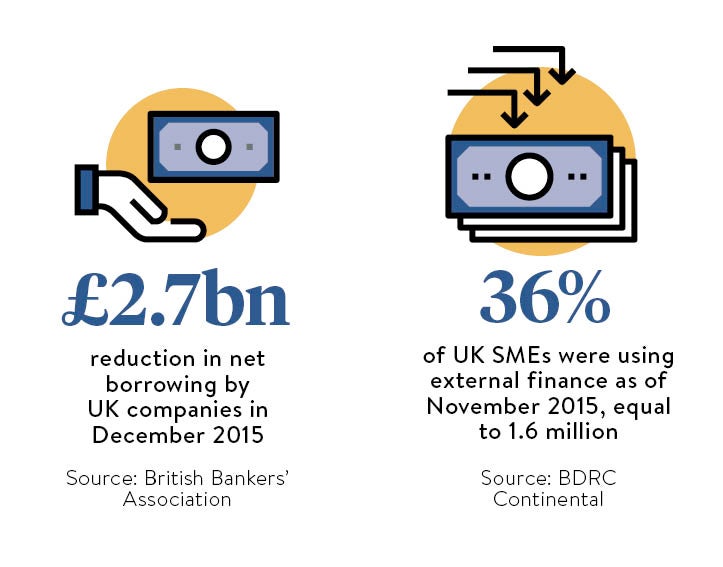

According to data from the British Bankers’ Association, net lending to businesses – the amount of new loans paid out compared with the amount paid off by customers – slumped by £2.7 billion in December.

While it does not break down the data by company size, similar figures from the Bank of England showed that net lending to SMEs fell by £300 million in December, after a modest rise the previous month.

“The sharp fall in lending at the end of last year was a timely reminder that accessing finance remains a major issue for businesses,” says Suren Thiru, UK economic adviser at the British Chambers of Commerce.

“Young, high-growth firms in particular are still facing a real struggle to get the finance they need to reach their full potential. More must be done to improve SME access to non-equity finance and to ensure that the British Business Bank has sufficient funding to help support some of our most promising young firms on their growth journey.”

The fall in net lending at the end of last year came despite the introduction of the Bank of England and Treasury’s Funding for Lending Scheme (FLS) in 2012, which was originally designed to encourage banks and building societies to boost their lending to both households and businesses.

At the end of 2013, it was altered to focus mainly on business lending after borrowing by households recovered much more quickly than had been expected by policymakers.

While everyone waits for bank lending to businesses to get back on track this year, the ever-growing army of alternative funders is set to expand further in 2016

Further alterations were made to the flagship lending scheme to include asset-based lenders and most recently chancellor George Osborne announced in the Autumn Statement that the scheme would be extended for another two years.

“Now that credit conditions for households and large businesses have improved, it is right that we focus the scheme’s firepower on small businesses, which are the lifeblood of our economy,” Mr Osborne said.

[embed_related]

The FLS extension was announced alongside a package of measures to help boost lending to SMEs, including guaranteeing up to £500 million of bank lending to these firms, which the government is no doubt hoping will kick-start a fresh wave of corporate borrowing in 2016.

But while everyone waits for bank lending to businesses to get back on track this year, the ever-growing army of alternative funders, including crowdfunding, peer-to-peer lending and pension-led funding among others, is gathering pace and is set to expand further in 2016.

For example, Funding Circle, the peer-to-peer lender, which was set up by three Oxford University graduates to capitalise on the high street banks’ failure to lend to SMEs, recently reported that it passed the £1-billion lending milestone.

According to Samir Desai, its chief executive, more than half of this was lent in 2015 and investors are on track to lend a further £1 billion over the next 12 months, as marketplace lending proves to be the preferred option for small businesses looking to access finance.

The impact of public policy in 2016

Apart from whether funds are available from banks and alternative lenders, there are also several factors at play this year, which will impact SMEs’ decision to borrow money in the first place as well as choosing what to do with it.

The first is the prospect of policymakers at the Bank of England voting to lift interest rates from the record low of 0.5 per cent, where they have stood still since the depths of the downturn in 2009.

While there has been a succession of mixed signals on the timing of the first increase from the Bank of England, the latest steer from governor Mark Carney is that Britain is not ready for one.

As a result of comments by Mr Carney and some of his fellow dovish colleagues on the Monetary Policy Committee, analysts are predicting that a small rise would come at the end of 2016, while others believe that 2017 is much more likely.

Other factors at play, according to recent research from the Federation of Small Businesses, include the rollout of pension auto-enrolment and the new national living wage. Its members are also deeply worried about proposed mandatory quarterly tax reporting, which in its current form will add to the administrative burden of small firms and the self-employed.

2016 will certainly be an interesting year.

Lending slump