Will it be a happy new year for the UK banking sector? When the transition period of Britain’s exit from the European Union ends on January 1, business leaders and bankers alike will tiptoe into a post-Brexit reality. Enmeshed by confusing and in some cases yet-to-be-determined rules, they will be entering a new global banking landscape.

But given that financial institutions inside and outside Europe have been preparing for this day since the EU referendum on June 23, 2016, will things be markedly different?

Whatever happens, British banks and their European counterparts have had enough time to ready themselves for post-Brexit life. Admittedly, some details still need to be finalised, though Bank of England governor Andrew Bailey has been warning the largest UK lenders to plan for a no-deal Brexit since June.

Legally, there will be changes, if only slight to begin with, on a global scale. “As of January 1, banks located in the EU and the UK will have to operate in two separate regulatory and supervisory environments,” says Yves Mersch, a member of the European Central Bank’s executive board. “Providers of financial services between the EU and the UK will no longer enjoy the benefits of the single market.

“Many euro-area banks doing business across the Channel, as well as UK banks operating in the euro area, have made considerable progress in view of this event.” Mersh adds that most are “on track to finish their preparations” this year, but others “have much work to do”.

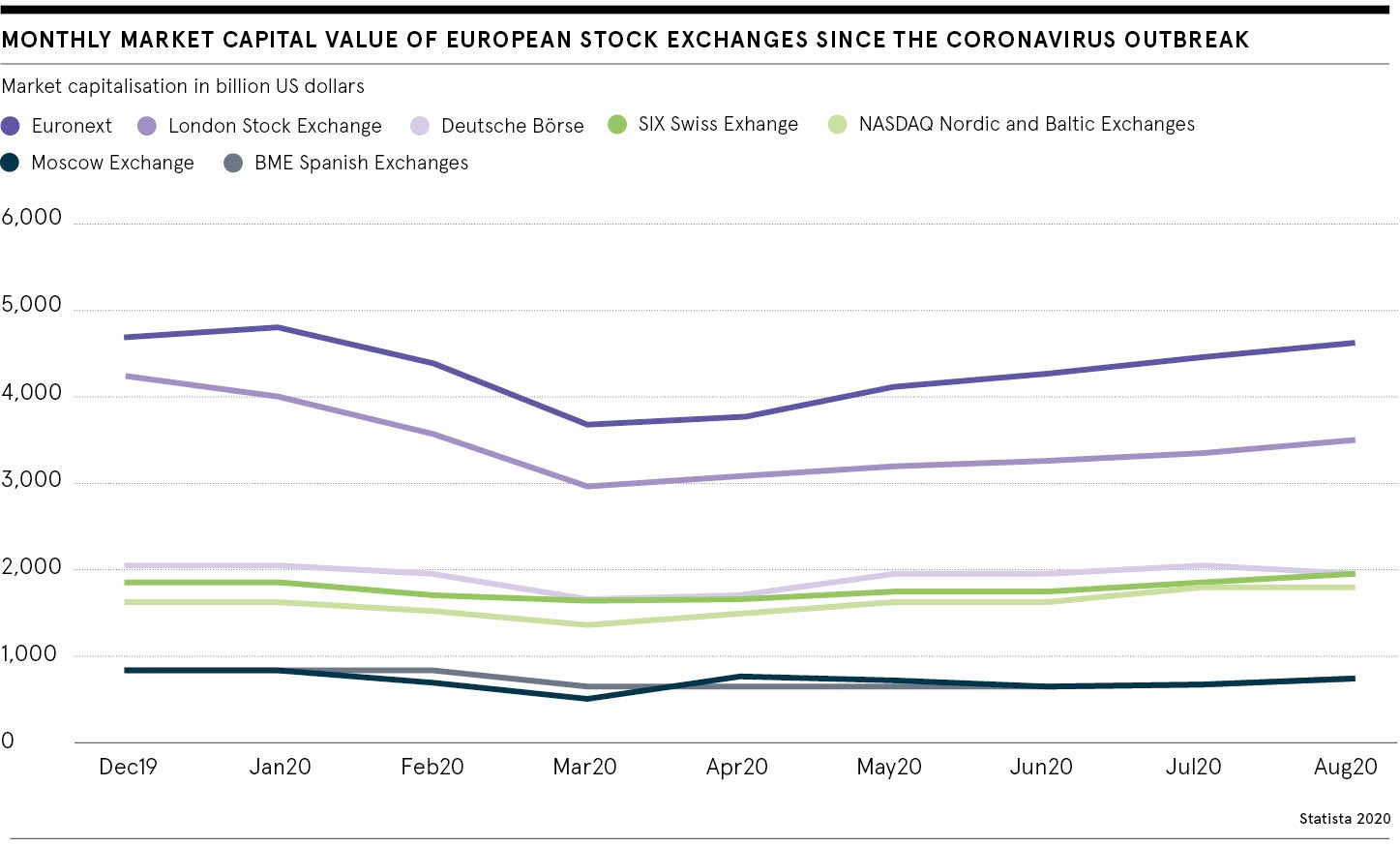

For the latter, the coronavirus fallout has disrupted post-Brexit plans. “Broadly speaking, the main priority for banks over the past few months has been tackling the multi-faceted consequences of the pandemic,” he says.

No excuse for banks to be unprepared

Indeed, the “C” word has obscured the “B” word since March, and although COVID-19 may provide a reason for the sluggish progress of Brexit negotiations, it is not a just excuse for banks to be ill-equipped. Many big players lined up their moves long ago.

EY calculates that banks and fund managers have committed to moving £1 trillion of assets out of the UK and into the EU because of Brexit. US lender JPMorgan Chase & Co., for

instance, is expected to shift around £180 million in assets to Germany. Further, it has ordered 200 staff to move out of London to other European cities including Paris, Milan, Madrid and Frankfurt, in the expectation that the UK and the EU will not firm up an agreement on financial services.

The UK has always been, and continues to be at least for now, a world leader in financial services

Considering the UK exports more than £26 billion in financial services to the EU, according to the Office for National Statistics, perhaps the global post-Brexit banking landscape may transform quicker if no deal is reached.

However, James Butland, vice president of global banking at cross-border fintech Airwallex, argues the “mass exodus” from London “has not happened to the extent so many were sure it would”. He says: “London remains an attractive place where people want to live and work. Equally, the ecosystem in London is truly global, like New York or Hong Kong, and has always been regarded as a crucial financial hub.

“The UK has always been, and continues to be at least for now, a world leader in financial services, eclipsing many of its EU rivals across the sector. And despite uncertainty around Brexit, one thing is clear: Europe will remain a leader within the global banking industry, mainly due to the strength of the euro as a currency.”

London has critical role to play

But Butland says ”a new leader needs to take London’s crown” within the region. He continues: “The European banking community may start to face geographical fragmentation, as the position to become the epicentre of the eurozone opens up. The race to become the financial capital of the EU seems to be between Paris, Frankfurt, Brussels and Amsterdam, with no winner yet in sight. Wherever this location may be, it should look to London to continue Europe’s legacy as a leader within the global banking economy.”

Alastair Holt, financial regulations partner at global law firm Linklaters, agrees. “Other European cities will not be as influential as London, at least in the short to medium term,” he adds. “London can play a critical role in bridging the East and the West, particularly given the increasing tensions we have seen between the world superpowers in those regions.

“The UK will still be a leading global financial centre, boosted by its language, time zone, the legal system, and the pre-existing ecosystem of financial institutions and suppliers, the vast majority of which will remain in the UK.”

Professor Brian Scott-Quinn, director of banking programmes at Henley Business School, is more cautious and believes the global banking landscape has been fragmented since the 2008 financial crash.

“Just as trading relationships between the major blocs – the United States, Europe and China – have been damaged in recent years, as well as the relationship between the UK and the rest of Europe, so globalisation of banking and finance has been in low gear now since the financial crisis,” he says. “Most UK banks that had plans for internationalisation or for building up their investment banking capabilities have since abandoned such plans.”

Contingency plans needed for uncertain year

Regardless, Holt argues that coronavirus is more of a threat to the banking sector’s future. “COVID-19 is clearly a worry, more so than Brexit,” he says.

Chris Ganje, chief executive and co-founder of Cardiff-based fintech AMPLYFI, which focuses on developing artificial intelligence for banking, expands upon this theme. “The banking sector should have already dealt with Brexit over the past two years with robust models in place to move on,” he says. “The fallout of COVID-19 is a major unknown. For example, any FCA Section 166 notice into how a bank handled crisis-related loan applications could cost it tens of millions of pounds to review.”

Additionally, Alessandro Hatami, co-author of Reinventing Banking and Finance, says it is hard to quantify the effect of Brexit at the moment. And he points out: “The impact of leaving the EU financial passporting scheme, making it harder for UK fintechs to serve European customers from the UK, is also not clear and won’t be until the final deal is negotiated.”

Butland at Airwallex concurs that 2021 will be pivotal in shaping the global banking landscape. “The next 12 months will certainly be interesting, as both the pandemic continues and the repercussions of a potential Brexit deal loom ahead,” he concludes.

“Whatever happens over the coming year, disruption lies ahead. Financial institutions will be making contingency plans for every possible eventuality.”

Brexit and COVID-10 accelerate move to digital

The United Kingdom European Union membership referendum was inevitable when David Cameron won the 2015 general election, having promised such a vote during his campaign. Coincidentally, 2015 was when branchless challenger banks Monzo and Revolut were founded, with Starling launching a year earlier.

While the direction of travel was established five years ago, the combination of Brexit and now COVID-19 has quickened the drive for older financial institutions to transform their business and operating models, because it’s clear: the future is digital.

Technology is enabling fintechs to enter the banking market, and thrive. Experts predict traditional banks will have to partner with tech organisations to keep pace with developments.

A study of 200 UK and European banking executives by Marqeta – an open-API card issuing and processing platform that MasterCard has recently invested in – found that in the wake of the coronavirus pandemic over three-quarters (78 per cent) of banks have been forced to change their future banking strategy.

Some 72 per cent of those surveyed are planning to grow the number of in-branch digital services, and two-thirds will invest more in digital banking and services. Further, nine in 10 respondents (89 per cent) says the COVID-19 situation has “drastically increased” the speed of change in banking from years to months.

Max Chuard, chief executive of Geneva-based banking software fintech Temenos, says: “Uncertainty is a catalyst for innovation. The 2020s were already set to be the decade for digital banking transformation. But now the coronavirus crisis has accelerated this process. It has made the need for advanced banking technologies – like artificial intelligence, cloud and SaaS – even greater.”

Defining moment for the banking industry

The Temenos CEO points to his organisation’s global survey that shows almost half of the respondents (45 per cent) say their strategic response to the rapidly changing banking landscape is to build a “true digital ecosystem”. He adds: “It’s a defining moment for the banking industry, and those who can harness the potential of digital technology will shape the future.”

Lee Edwards, vice-president in Northern Europe, the Middle East and Africa for computer software giant Adobe, thinks the same. “Banks have to ensure they keep pace with digital-first challenger banks, such as Monzo or Starling, to deliver new experiences that both enhance and complement their bricks-and-mortar branches,” he says. “This has included implementing new technologies within apps and websites that enable customers to perform tasks previously exclusive to the branch, like cashing cheques or remote meetings with advisors.”

This need to evolve banking operations provides an opportunity to streamline typically time-intensive tasks, such as setting up an account or applying for a loan, Edwards says. “As an example, TSB implemented digital signature technologies using Adobe Sign to allow customers to carry out important processes from their own home, moving over 15,000 account sign-ups that would normally require a trip to the branch,” he adds.

That convenience will be central to winning customers, believes Aaron Archer, chief executive and founder of London-headquartered challenger bank Finndon. “Digital banks will see a major increase in their market share compared to high street banks, due to their lack of flexibility to adapt to market conditions, and customers will be seeking greater opportunities to save.”

He wouldn’t be surprised if big tech firms, including Apple and Google, begin to “offer banking products to their customer base to create a robust ecosystem”. Archer adds: “You will see an increase of mergers and acquisitions between tech firms and traditional banks looking to stay relevant.”

Sophia La Vesconte, a fintech lawyer at Linklaters, agrees. “With increasing digitalisation, we are likely to see a growth in outsourcing arrangements between the financial sector and technology service providers.” However, she warns: “Regulators across the globe are quite concerned about the sector becoming overly dependent on a small number of – unregulated – technology companies.”

Will it be a happy new year for the UK banking sector? When the transition period of Britain’s exit from the European Union ends on January 1, business leaders and bankers alike will tiptoe into a post-Brexit reality. Enmeshed by confusing and in some cases yet-to-be-determined rules, they will be entering a new global banking landscape.

But given that financial institutions inside and outside Europe have been preparing for this day since the EU referendum on June 23, 2016, will things be markedly different?