Choosing a new car is a big decision, so no wonder we take our time over it. Forty per cent of over-55s will take more than a week to come to a conclusion.¹

Choosing a new car is a big decision, so no wonder we take our time over it. Forty per cent of over-55s will take more than a week to come to a conclusion.¹

But just under a third (32 per cent) of the same age group spends less than a week making a decision about their pension,² despite the fact that we might have to live with the consequences of that decision for 30 years or more.

As a nation, we are not spending enough time thinking about how we want to use our pension. Pensions might not be as glamorous as fast cars, but unless we spend time on the vital task of planning our retirement finances, we run the risk of not having enough money in later life.

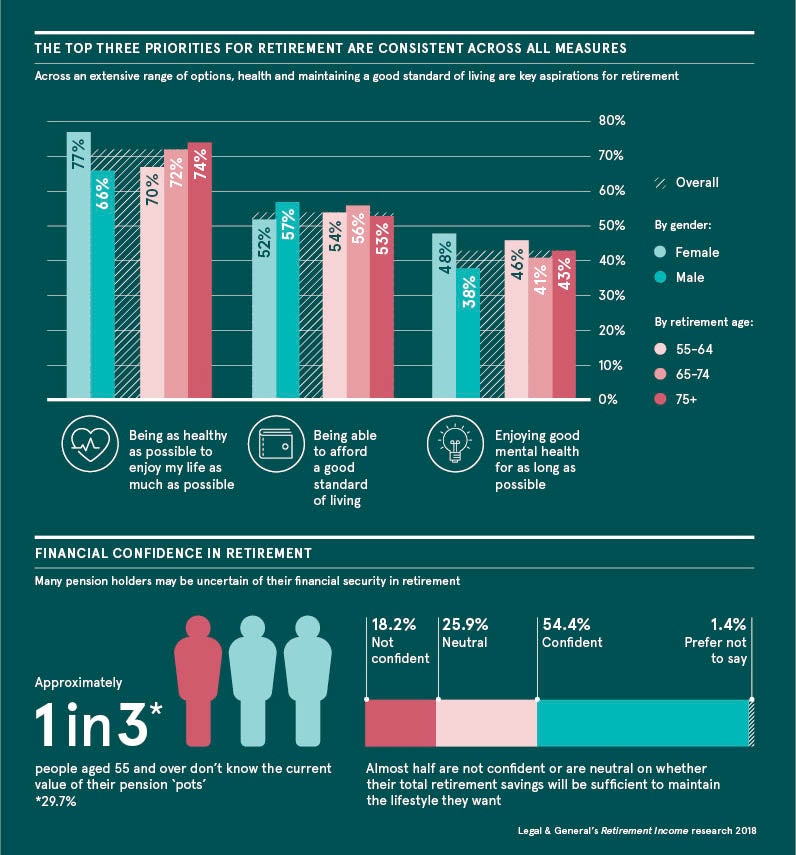

Nobody wants to face poverty in old age and more than half of us see financial security as our top priority in retirement.³ But, just as it’s hard to connect a couple of biscuits now to an inability to fit into next summer’s holiday clothes, most of us struggle to connect making the effort now with a financially healthier retirement.

Part of the problem is it’s hard to see clearly when it comes to such long-term decisions. After all, retirement has changed a lot; we expect more from the last third of our life than ever before and today’s retirees are a very long way from having one foot in the grave.

They may be healthier than their parents were and they may well be playing a pivotal role in the lives of children or grandchildren. They still have ambitions and want to take on new challenges; retirement is not the cliff edge it used to be. It is something much more flexible and our pensions need to reflect that.

That’s partly what Pension Freedom was all about, allowing consumers to choose the retirement products that would best meet their needs rather than prescribing a one-size-fits-all approach. Now, you can choose to take cash, buy a guaranteed income for life (an annuity), leave it invested taking out chunks of your pension savings when you need it (income drawdown) or a combination of these.

But many customers don’t know about some of the fundamental factors that can impact how much money we have in retirement. More than a quarter of us (27 per cent) don’t realise we have to pay tax on our pension savings if we take the money as cash.

Just over a quarter of us don’t expect to pay tax on our pension income.⁴ That lack of simple awareness could cost us dearly, but can be caught early with a bit of research. Many of us put off planning because pensions are seen as too confusing and it’s true that too much choice can be overwhelming. The pensions industry must also bear some of the blame; jargon is still too common and plain talking all too rare.

Conversations need to be about retirement goals and plans, not about products. If the industry can do this, improving communication with customers and providing them with the support they need to make informed decisions, then everyone will be in a much better place to enjoy a more prosperous retirement.

But there’s no one-size-fits-all answer when it comes to retirement. Each of us has a unique set of circumstances and it’s not just your financial profile – your current savings, where your money is invested and your appetite for risk – that determine the best options. It’s also your life expectancy, which may be higher than you think, or if you have a medical condition or made lifestyle choices, such as smoking which might lower life expectancy, but mean you qualify for a higher annuity. A good adviser can help you plan, but only if you are honest about where you are now and really assess your circumstances.

Today’s financial landscape means we are all responsible for making sure our pension pots will last through our retirement. Most of us want clarity and certainty in later life, but the choice is yours: spend some time now and aim for a more prosperous retirement.

To start your planning please visit www.legalandgeneral.com/retirement

www.pensionsadvisoryservice.org.uk

1, 2, 3, 4 Legal & General’s Retirement Income research 2018

Top tips to get started

Sometimes we fail to plan our retirement because the job is just too big and scary. Use some behavioural tricks to get started.

Set a timer and focus on it for just 15 minutes or as long as it takes to drink a cup of tea. Then repeat a few times a week.

Break the job into small steps: get out the paperwork, read three guidance articles online, book an appointment with an adviser.

Reframe the problem: not “I ought to plan” but “I choose to plan”.

Build a list of reasons why you want to do this: to avoid poverty in later life, to feel secure about your future, to understand enough to avoid being ripped off.